If you’re not yet a member, join now for access to a whole lot more!

28 October 2025

Spark Limited (SPK)

The company will hold its Annual Shareholders Meeting at 9.30am Friday 7 November 2025.

The location is the Conference Centre, Ground Floor, 50 Albert Street, Auckland.

You can also join the meeting online at this link.

Company Overview

The company is the largest telco in New Zealand. It employs over 4,000 people in 24 business hubs, 69 retail stores, its data centres and its headquarters. It has over 2.6 million mobile connections, over 660,000 broadband connections with 99% of the country on the 4G network. It is rolling out the 5G network at pace with over 50% of the population having access to 5G.

In August 2025, the company announced the sale of 75% of its data centres to Pacific Equity Partners.

There have been a number of Board changes. Lindsay Wright was appointed to the Board 1 August 2025 with Vince Hawksworth and Tarek Robbiati appointed 1 October 2025. Gordon MacLeod retired from the Board 1 September 2025 and Sheridan Broadbent retired 1 October 2025. The Chair Justine Smyth who has served since 2011 and is standing for re-election has indicated she will retire from the Board within 12 months to allow for an orderly transition.

+=========================================================================================

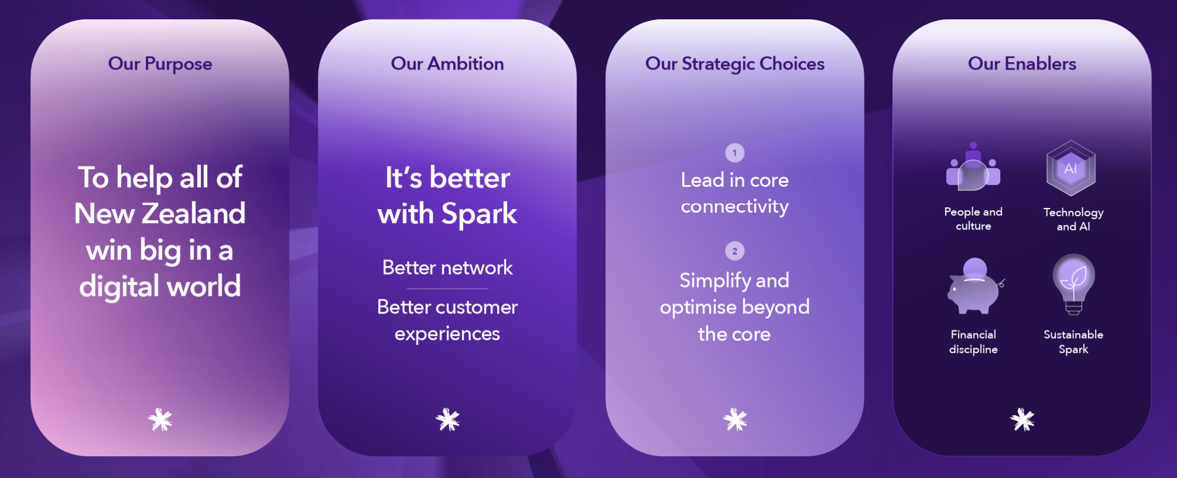

Current Strategy

The 5 year strategy to 2030 is at this link. A summary is shown in the image below.

Previous Year Shareholder Meeting

NZSA recorded the following key items at last year’s annual shareholder meeting:

- FY24 was a challenging year for the company and despite some green shoots, challenges still remained for the result in FY25.

- Revenue was down 14% at $3,861 million.

- The Chair’s final remarks re-iterated the share price was “not where we want it to be” and that the board “believe in this business “.

The meeting report is available at this link.

Disclaimer

To the maximum extent permitted by law, New Zealand Shareholders Association Inc. (NZSA) will not be liable, whether in tort (including negligence) or otherwise, to you or any other person in relation to this document, including any error in it.

Forward looking statements are inherently fallible.

Information on www.nzshareholders.co.nz and in this document may contain forward-looking statements and projections. For any number of reasons, the future could be different – potentially materially different. For example, assumptions may be wrong, risks may crystallise, unexpected things may happen. We give no warranty or representation as to any future financial performance or any other future matter. We may not update our website and related materials for changes.

There is no offer or financial advice in our documents/website.

Information included on www.nzshareholders.co.nz and in this document is for information purposes only. It is not an offer of financial products, or a proposal or invitation to make any such offer. It is not financial advice and does not take into account any person’s individual circumstances or objectives. Prior to making any investment decision, NZSA recommends that you seek professional advice from a licensed financial advice provider.

There are no representations as to accuracy or completeness.

The information, calculations and any opinions on www.nzshareholders.co.nz and in this document are based upon sources believed reliable. The NZSA, its officers and directors make no representations as to their accuracy or completeness. All opinions reflect our judgement on the date of communication and are subject to change without notice.

Please observe any applicable legal restrictions on distribution

Distribution of our documents and materials on www.nzshareholders.co.nz (including electronically) may be restricted by law. You should observe all such restrictions which may apply in your jurisdiction.

Key

The following sections calculate an objective rating against criteria contained within NZSA policies.

|

Colour |

Meaning |

|

G |

Strong adherence to NZSA policies |

|

A |

Part adherence or a lack of disclosure as to adherence with NZSA policies |

|

R |

A clear gap in expectations compared with NZSA policies |

|

n/a |

Not applicable for the company |

Governance

NZSA assessment against its key policy criteria are summarised below.

|

G |

Directors Fees: Excellent disclosure. The Board Charter notes that “The Board may determine that additional allowances be paid to a Director, as appropriate, to reflect additional services provided to the Company by that Director,” although no such payments are disclosed for FY25.

|

G |

Director Share Ownership: Directors are expected to accumulate the equivalent of one year’s fees over their first three years. While NZSA encourages share ownership by independent directors, it does not support compulsion as this reduces the pool of available Directors, may compromise independence, and removes the ‘market signal’ associated with share purchases.

The timeframe of three years to achieve the target implies a 33% purchase rate, meaning that a Board applicant would require existing wealth to serve on the Board. NZSA does not believe that ability is not defined solely by wealth. In this context, however, we observe that the Chair holds discretion to waive the requirement depending on a director’s personal circumstances.

|

G |

CEO Remuneration: The company discloses its remuneration policy on its website, which includes an overview of the remuneration philosophy applicable to the company. The Human Resources and Compensation Committee is responsible for implementing the policy.

Incentives: The CEO is paid a short-term incentive (STI) in cash and a long-term incentive (LTI) by way of share options.

NZSA encourages fulsome disclosure in relation to any incentive payments made to the CEO, including disclosure of measures (or measure ‘groups’), weightings, targets, and the level of achievement versus target for each component associated with any awards. This methodology is supported by the NZX Remuneration Reporting Template.

Spark offers excellent disclosure of the methodology for both the STI and LTI awards. The STI is based on EBITDAI, Customer Experience metrics and Digital infrastructure revenue. Weightings and the level of achievement are both shown. We note that no STI payment was made, on the basis that the EBITDAI ‘gate’ was not met.

The company discloses both the LTI awarded and paid, removing the ‘conflation’ between the timing differences associated with remuneration earned (or awarded) compared with remuneration paid (or vested). The LTI awarded in FY22 (vesting in FY25) was based on an absolute shareholder return. No options were issued as the vesting conditions were not met. We note the LTI award for FY25 will vest on the basis of Scope1-3 emission targets (12.5%) and gender pay gap (12.5%), with shareholder return remaining as the major metric (75%).

The STI and LTI awards (at targets) are 75% each of the base salary, with the ability to outperform on the STI. NZSA prefers a weighting towards LTI to ensure the CEO’s interests are aligned with the long-term interests of shareholders.

The company discloses the gender pay gap but not the CEO/employee remuneration ratio.

Golden Parachutes: In the interests of transparency, NZSA believes there should be explicit disclosure around the severance terms and notice periods associated with the CEO, including whether specific termination payments are offered.

As regards termination payments, while NZSA does not generally support such payments, we are pleased to see the clear disclosure offered by Spark, highlighting a 3-month notice period by the company and an associated 9-month payment. This provides a disclosed ‘cap’ on the total possible payment.

We note that Spark clearly discloses the ‘without cause’ notification period and associated termination payment for the CEO, however, this results in a significant termination payment, beyond that generally offered to other staff. Nonetheless, NZSA appreciates the disclosure offered.

|

G |

Director Independence: A majority of Directors are independent.

|

G |

Board Composition: Spark discloses a comprehensive skills matrix that provides assurance to shareholders as to the relationship of individuals on the Board to the governance skills required.

The company is one of very few that participates in the IoD’s Future Director programme (or similar) designed to develop and mentor the next generation of Directors. NZSA expect NZX50 companies to participate as part of a responsibility to develop and mentor the next generation of Directors.

We are pleased to note following our comments last year, the CEO/Managing Director is no longer a member of the Nominations and Corporate Governance Committee. NZSA considered this could create a conflict of interest as regards the nomination and appointment of new Directors. Whilst it is appropriate the CEO is consulted, NZSA believes the CEO should not take part in the appointment process.

The nature of the company’s board indicates a commitment to thought, experiential and social diversity, with relevant experience for Spark.

|

G |

Director Tenure: NZSA looks for evidence of ongoing succession or ‘staggered’ appointment dates that reduce the risks associated with effective knowledge transfer in the event of succession. We also prefer a term maximum of 9-12 years, unless there are exceptional circumstances that may apply.

With Justine Smyth announcing her intention to retire from the Board within 12 months, Director appointment dates range from 2019 to 2025. NZSA notes that the company’s likely director succession plans have been subject to some pressure caused by unexpected resignations; in this context, we are supportive of Smyth’s clear signal as to her future tenure.

|

G |

ASM Format: Spark Limited is holding a ‘hybrid’ meeting, (i.e., physical, and virtual), a format preferred by NZSA as a way of promoting shareholder engagement while maximising participation.

|

G |

Independent Advice for the Board & Risk Management: NZSA looks for evidence, through disclosures, that a Board has access to appropriate internal and external expertise to support board assurance and decision-making activities. We also look for evidence that Boards are across their risk management responsibilities.

The Board Charter states that Directors are entitled to seek independent external advice at Spark’s expense, with the prior approval of the Chair. Board members are also able to access internal staff as required. The internal audit plan is overseen by the Audit Committee and the Company Secretary is accountable to the Board as disclosed in the Annual Report.

Spark offers comprehensive disclosure of the key strategic, business, operational and financial risks that impact the business, as well as mitigations. There is also thorough disclosure of its risk management and governance processes. We note that Spark aligns with COSO ERM and ISO 31000 standards related to risk management. The company has published a separate 26-page Climate Related Disclosures Report.

Audit

NZSA assessment against its key policy criteria are summarised below.

|

G |

Audit Independence: Good disclosure.

|

G |

Audit Rotation: The company ensures the Lead Audit Partner is rotated at 5 years as required by the NZX Listing Rules. The Notice of Meeting discloses the date of appointment of the Audit firm (Deloitte, 2020) and that Mr Jason Stachurski was the lead audit partner for the financial year ending 30 June 2025. In line with the audit partner rotation policy Ms Melissa Collier has been appointed the lead audit partner for the financial year ending 30 June 2026

Environmental Sustainability

|

G |

Overall approach: Spark continues to report using the Integrated Reporting (IR) Framework, with its climate disclosures now presented in a standalone Climate-Related Disclosures (CRD) report for FY25, published alongside the Annual Report. This is a progression from FY24, where the CRD was integrated into the Annual Report. Spark’s climate reporting is now aligned to the Aotearoa New Zealand Climate Standards, and the company has applied four adoption provisions during FY25.

|

G |

Sustainability Governance: Spark’s board retains responsibility for climate-related risks and opportunities, supported by the Audit and Risk Management Committee, which reviews climate risk as part of principal risk oversight. The board has also established a Due Diligence Committee to oversee the preparation of climate disclosures, now in its second year of operation. Spark discloses a board skills matrix, which includes sustainability competencies. There are also dedicated resources responsible for climate matters, including a Corporate Relations and Sustainability Director, a Sustainability Lead, and an Emissions Reduction Steering Committee.

|

G |

Strategy and Impact: Spark confirms that climate considerations are integrated into its SPK-30 business strategy, particularly through investment in network resilience, energy efficiency and renewable electricity sourcing. The company reiterates that it does not require a significant shift in business model to adapt to climate risks, reflecting its relatively low operational emissions profile and the essential nature of telecommunications infrastructure. Spark states it does not currently have a standalone transition plan, but transition actions are embedded within strategic planning processes. NZSA notes this approach is acceptable provided Spark continues to evolve disclosures consistent with XRB transition planning expectations.

|

G |

Risk and Opportunity: The company identifies supply chain disruption, network resilience, energy security, and regulation as key exposures. Spark also provides a section on climate-related opportunities, including decarbonisation solutions enabled by technology. Each risk and opportunity is accompanied by management actions, which improve transparency.

|

G |

Metrics and Targets: Spark discloses Scope 1 and 2 emissions, together with partial Scope 3 categories, consistent with adoption provisions. Emission trends are reported from FY2020 to FY2025, showing year-on-year performance against a science-based target to reduce Scope 1 and 2 emissions by 56% by FY2030. Spark has also committed to having 70% of suppliers (by spend) set science-based targets by FY2026, providing a pathway for Scope 3 engagement. Environmental performance continues to be financially incentivised, with ESG metrics comprising 12.5% of long-term incentive weighting for the CEO and Leadership Squad.

|

G |

Assurance: Spark obtains independent limited assurance from Deloitte over its FY25 GHG inventory and selected climate disclosures, consistent with NZSA expectations at this stage of climate reporting maturity.

Ethical and Social

NZSA assessment against its key policy criteria are summarised below.

|

G |

Whistleblowing: Good disclosure.

|

G |

Political Donations: No donations were made.

Financial & Performance

|

Policy Theme |

Assessment |

|

Capital Management |

G |

|

Takeover or Scheme |

n/a |

Sparks’s share price fell from $3.03 to $2.41 (as of 14th October 2024) over the last 12 months – a 20% decline. This compares unfavourably with the NZX50 which rose 5% in the same period. The capitalisation of SPK is $4.6b placing it 16th out of 115 companies on the NZX by size and makes it a large company.

|

Metric |

2021 |

2022 |

2023 |

2024 |

2025 |

Change |

|

Revenue |

$3,593m |

$3,720m |

$4,491m |

$3,861m |

$3,725m |

-4% |

|

EBITDAI |

$1,124m |

$1,150m |

$1,722m |

$1,163m |

$1,053m |

-9% |

|

EBITDAI Margin |

31% |

31% |

38% |

30% |

28% |

-6% |

|

NPAT |

$384m |

$410m |

$1,135m |

$316m |

$252m |

-20% |

|

EPS1 |

$0.206 |

$0.219 |

$0.615 |

$0.174 |

$0.133 |

-23% |

|

PE Ratio |

23 |

23 |

8 |

18 |

18 |

|

|

Capitalisation |

$8.9 |

$9.5b |

$8.7b |

$5.7b |

$4.6b |

-20% |

|

Current Ratio |

b0.98 |

1.30 |

1.27 |

1.01 |

1.35 |

34% |

|

Debt Equity |

1.74 |

1.84 |

1.31 |

1.92 |

1.98 |

3% |

|

Operating CF |

$858m |

$841m |

$800m |

$764m |

$680m |

-11% |

|

Operating CF (cps) |

$0.46 |

$0.45 |

$0.43 |

$0.42 |

$0.36 |

-11% |

|

NTA Per Share1 |

$0.34 |

$0.34 |

$0.61 |

$0.41 |

$0.38 |

-7% |

|

Dividend1 |

$0.25 |

$0.25 |

$0.27 |

$0.275 |

$0.25 |

-9% |

1 per share figures based off actual shares at balance date (not weighted average)

Most metrics we follow for Spark declined further in 2025 and this was reflected in a falling share price, which fell another 20%.

Revenues were down 4% to $3.7b, and coupled with a lower EBITDAI margin of 28%, meant decreased EBITDAI of $1,053m and a subsequent decrease of 20% in NPAT to $252m. EPS of $0.133 were reported.

Following on from these reduced results, SPK also reduced their fully imputed dividends to $0.25.

Spark pay dividends well in excess of EPS, and utilises operating cashflows to allow these payments. This is a metric we will continue to watch closely. We also note that SPK have a large depreciation expense of $590m. NZSA has discussed the longer-term sustainability of the dividend policy with the company. We acknowledge both the linking of future dividends to free cashflow and the reduced capex outlook following the recent partnership established in relation to SPK’s former data centres.

The company is in a financially sound position, with a current ratio at 1.35 meaning they can meet requirements as they fall due. The company retired some debt during FY25 with total debt now standing at $1,482m. This debt reduction has been supported by the sale of Connexa. However, the debt equity ratio rose to a high 1.98, a ratio slightly elevated due to the material amount of lease liabilities on the balance sheet.

SPK has high operating cashflows of $680m, representing $0.36 cents per share and has a low NTA of $0.38. Shares consistently trade at large premiums to NTA, reflecting future cashflow expectations.

The company released an investor presentation in conjunction with their annual results and provided some forward looking guidance. They expect EBITDAI of between $1,020m and $1,080m and expect to pay 100% of free cash flow (FCF) in dividends.

The share register is widely held by a variety of institutions and individuals.

Resolutions

1. To elect Lindsay Wright as an Independent Director.

Lindsay Wright was appointed to the Board 1 August 2025 and is therefore required to offer herself for election. She has more than 35 years of executive experience in the financial services sector, both within New Zealand and internationally. She has held senior management roles at leading global asset management firms covering commercial operations including business development and stakeholder management, strategy, investment management, finance, capital markets, and risk and capital management. Her governance experience spans 14 years, serving on boards of both listed and private companies. She currently holds directorships with NZX Limited, Milford Asset Management and ASX-listed Navigator Global Investments. Her previous board appointments include Kiwibank and the Guardians of New Zealand Superannuation, where she was Deputy Board Chair and Audit Committee Chair.

We will vote undirected proxies IN FAVOUR of this resolution.

2. To elect Tarek Robbiati as an Independent Director.

Tarek Robbiati was appointed to the Board 1 October 202 and is therefore required to offer himself for election. His has held leadership roles in global telecommunications, technology, and financial services large-scale organisations. Tarek has served as CFO at Sprint Corporation, and Group Managing Director at Telstra International Group. He is currently CFO at NYSE listed Pure Storage, and a director on the Board of Digicel. His listed company governance experience includes serving on the Boards of TelstraClear New Zealand, Hewlett Packard Enterprise Financial Services, CSL Limited Hong Kong, and Australia-Japan Cable Limited Bermuda

We will vote undirected proxies IN FAVOUR of this resolution.

3. To elect Vince Hawksworth as an Independent Director.

Vince Hawksworth was appointed to the Board 1 October 2025 and is therefore required to offer himself for election. He has over 18 years’ Chief Executive experience in utility and infrastructure businesses across New Zealand and Australia, having most recently served as Chief Executive of Mercury Energy, and prior to that of Trustpower New Zealand. Vince is currently a director on the Board of Powerco, a Board Trustee of the Starship Foundation, and an Advisor to Datagrid New Zealand.

We will vote undirected proxies IN FAVOUR of this resolution.

4. To re-elect Jolie Hodson as a Non-Independent Director.

Ms Jolie Hodson was appointed to the Board 23 September 2019 and is the CEO. She joined Spark in 2013 as Chief Financial Officer and held the roles of CEO Spark Digital and Customer Director before being appointed CEO on 1 July 2019. Prior to joining Spark Jolie worked for 20 years in a range of senior roles for the Lion Group and Deloitte

We will vote undirected proxies IN FAVOUR of this resolution.

5. To re-elect Justine Smyth as an Independent Director.

Justine Smyth was appointed to the Board in December 2011 and became Chair in 2017. She has experience in governance, mergers and acquisitions, taxation, and the financial performance of large corporate enterprises as well as small and medium enterprises (SMEs). Her background is in finance and business management, having been a Partner with Deloitte and Group Finance Director at Lion Nathan. Justine is currently Chair of Mondiale VGL Limited and the Breast Cancer Foundation New Zealand and a former director of Auckland International Airport Limited. Justine has a Bachelor of Commerce from the University of Auckland and is a Fellow of Chartered Accountants of Australia and New Zealand and a Chartered Fellow of the Institute of Directors. In 2020 Justine was appointed a Companion of the New Zealand Order of Merit for services to governance and women.

On the basis of her clear intention relating to her future tenure, we will vote undirected proxies IN FAVOUR of this resolution.

6. That the Board is authorised to fix the auditor’s remuneration for the coming year.

This is an administrative resolution.

We will vote undirected proxies IN FAVOUR of this resolution.

Proxies

You can vote online or appoint a proxy at https://vote.cm.mpms.mufg.com/SPK/

Instructions are on the Proxy/voting paper sent to you.

Voting and proxy appointments close 9.30am Wednesday 5 November 2025.

Please note you can appoint the Association as your proxy. We will have a representative attending the meeting.

The Team at NZSA